Comprehensive Analysis of Beverage Consumption in India: Market Overview, Key Players, and Production Landscape in 2025

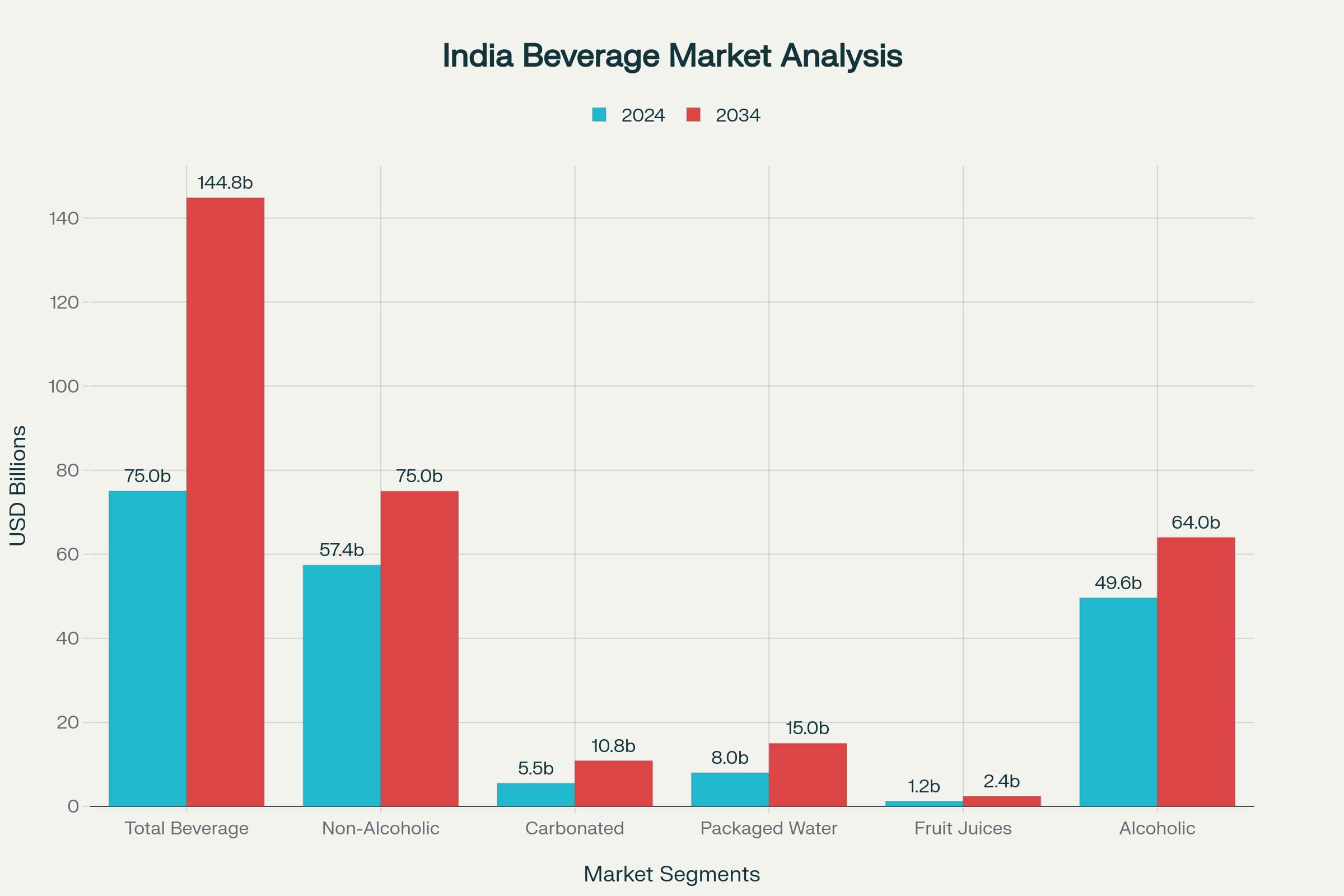

India’s beverage industry represents one of the world’s most dynamic and rapidly expanding markets, valued at USD 75.01 billion in 2024 and projected to reach USD 144.82 billion by 2034, growing at a robust CAGR of 6.8%. This comprehensive analysis examines the country’s beverage consumption patterns, major industry players, manufacturing infrastructure, and market dynamics that position India as the fifth-largest beverage market globally.

India Beverage Market Size Analysis: Current vs Projected Growth (2024-2034)

Market Size and Consumption Trends

Overall Market Dynamics

The Indian beverage market encompasses both alcoholic and non-alcoholic segments, with non-alcoholic beverages accounting for USD 57.4 billion in 2024. The market demonstrates strong growth potential despite relatively low per capita consumption compared to global standards. India’s per capita soft drink consumption stands at merely 5-6 bottles annually, significantly lower than Pakistan’s 17 bottles, Thailand’s 73 bottles, and Mexico’s 605 bottles.

Consumption Patterns and Growth Drivers

Recent market research indicates that Indian household soft drink consumption has surged past 50% penetration in FY24, with the average household expanding consumption by 250ml over the past two years9. This growth is driven by several key factors:

- Urbanization and Rising Disposable Income: Growing middle-class population with increased purchasing power

- Health Consciousness: Shift toward functional beverages and low-sugar alternatives

- Climate Impact: India’s tropical climate driving consistent demand for refreshing beverages

- Rural Penetration: Expanding distribution networks reaching tier-2 and tier-3 cities

Segment-wise Market Analysis

Hot Drinks dominate the Indian beverage landscape, accounting for the highest consumption volume in Q3 2024, with hot tea leading the category. The bottled water segment shows the strongest growth trajectory with an expected CAGR of 8.5%, while fruit juices demonstrate the highest growth potential at 10.2% CAGR.

Top 10 Beverage Companies in India

1. Varun Beverages Limited (VBL)

VBL stands as India’s largest franchisee bottler, operating 48 manufacturing facilities globally (34 in India). As the second-largest PepsiCo franchisee worldwide outside the US, VBL accounts for over 90% of PepsiCo’s beverage sales volume in India. The company reported net revenues of ₹20,007.7 crore in 2024, with production reaching 1,124 million cases annually.

Key Manufacturing Locations:

- Major Plants: Greater Noida (2 facilities), Kosi, Sathariya (2 facilities), Bazpur, Jainpur, Hardoi (UP); Bhiwadi, Jodhpur (Rajasthan); Nuh, Panipat (Haryana)

- Recent Expansions: Gorakhpur (2024), Prayagraj (2025), Supa Maharashtra (2024), Khordha Odisha (2024)

- Production Capacity: Significant expansion expected to boost peak month capacity by 45% over 2022 levels

2. Hindustan Coca-Cola Beverages (HCCB)

HCCB operates as Coca-Cola’s largest bottling partner in India, running 16-18 owned plants and covering approximately 65% of Coca-Cola system operations. The company manages an extensive distribution network spanning over 1 million outlets.

Manufacturing Infrastructure:

- Key Locations: Karnataka (Bidadi, Hospet), Maharashtra (Thane), Gujarat (Sanand, Kheda), Andhra Pradesh (Guntur), Uttar Pradesh (Dasna), West Bengal (Jalpaiguri, Shiliguri), Jharkhand (Jamshedpur)

- Recent Investments: New facilities planned in Gujarat, Telangana, and Maharashtra

- Production Focus: Sparkling beverages, still beverages, and packaged water under Coca-Cola trademarks

3. United Breweries Limited

India’s largest beer company with over 40% market share in the brewing sector. The company operates 79 distilleries and bottling units across India, with Kingfisher being the flagship brand.

Operational Network:

- Headquarters: Bangalore, Karnataka

- Manufacturing Presence: Karnataka, Andhra Pradesh, Goa, Kerala, Telangana, Punjab, Haryana, West Bengal, Rajasthan, Maharashtra, Odisha

- Ownership: 61.5% owned by Heineken since 2021, making it a top Heineken operating company globally31

4. Tata Consumer Products Limited

World’s second-largest tea manufacturer and distributor, Tata Consumer Products operates 10+ tea packaging plants with annual tea production of 60 million kg. The company manages 54 tea estates across India and Sri Lanka.

Production Infrastructure:

- Gopalpur Plant: Largest tea packaging facility producing 60 million kg annually by 2024-25

- Key Locations: Assam (Nonoi, Kellyden), West Bengal (Dam Dim, Kolkata), Kerala (Munnar), Odisha (Gopalpur)

- International Operations: UK, US, Canada with significant tea and coffee facilities

5. Parle Agro Private Limited

India’s largest domestic beverage company operating 84 state-of-the-art manufacturing facilities with over 5,500 employees. The company processes 2,10,000 MT of fruits annually, making it responsible for approximately one-third of India’s fruit pulp production.

Manufacturing Capabilities:

- Frooti Production: Increased mango consumption 150-fold from initial 1,000 MT to 1,50,000 MT annually

- Global Presence: Operations in over 50 countries with facilities in Bahrain and Angola

- Product Range: Fruit drinks, sparkling beverages, packaged water, and dairy-based beverages

6. Bisleri International

India’s leading bottled water company operating 150 manufacturing plants (13 owned, 137 co-packer arrangements) with a network of 6,000 distributors and 7,500 distribution trucks. The company dominates the ₹8,000 crore domestic bottled water market.

7. Amul (GCMMF)

World’s largest farmer-owned dairy cooperative with 98 processing plants and total annual milk processing capacity of 500 lakh litres. GCMMF handles 310 lakh litres of milk daily and reported turnover of ₹59,445 crore in FY24.

8. Mother Dairy

Market leader in Delhi-NCR’s branded milk segment, Mother Dairy operates 3 main plants with production capacity of 4.6 million litres per day. The company is investing ₹600 crore in new fruit and vegetable processing plants in Gujarat and Andhra Pradesh.

9. PepsiCo India Holdings

Operates primarily through its VBL partnership, PepsiCo maintains its presence across 27 states and 7 union territories in India. The company focuses on both beverages and snacks, with beverages accounting for a significant portion of operations through VBL.

10. Reliance Consumer Products (Campa Cola)

Newest major entrant in the beverage market, Reliance acquired Campa Cola in August 2022 and has rapidly expanded with 2 operational plants and ambitious expansion plans. The Guwahati facility produces 10 crore litres of CSD and 18 crore litres of packaged water annually.

Also Reliance Campa cola has tied up with various bottlers across the country for manufacturing Campa Cola.

Most Sold Beverage Brands in India

Carbonated Soft Drinks Market Leadership

Thums Up dominates as India’s most sold beverage brand, holding a decade-high market share of 20% in the carbonated drinks segment5657. The homegrown cola brand achieved this milestone through its distinct positioning as a “strong and masculine brand” with taste profiles suited to Indian palates56.

Top Beverage Brands by Market Share

- Thums Up (Coca-Cola): 20% market share, $1 billion annual sales (first Coca-Cola India brand to achieve this milestone)

- Sprite (Coca-Cola): 15% market share in lemon-lime segment

- Coca-Cola: 12% market share in cola category

- Mountain Dew (PepsiCo): 10% market share in citrus segment

- Kingfisher Beer (United Breweries): 40% market share in beer segment

Market Dynamics and Brand Performance

The top four soft drink brands include three Coca-Cola brands (Thums Up, Sprite, Coca-Cola) and one PepsiCo brand (Mountain Dew). Notably, Pepsi’s market share has declined to less than 5%, while Coca-Cola and PepsiCo combined control approximately 95% of the soft drinks market.

Segment-wise Brand Leadership

In the fruit beverage category, Frooti maintains its position as India’s largest-selling mango drink with 25% market share. The beer segment is dominated by Kingfisher with over 40% market share, making it India’s most consumed alcoholic beverage.

Production Capacity and Manufacturing Infrastructure

Geographic Distribution of Manufacturing

The beverage manufacturing landscape in India shows strategic geographic distribution to optimize logistics and market reach:

- Northern Region: Dominated by VBL facilities in UP, Haryana, Punjab, and Rajasthan

- Western Region: Strong presence of HCCB, Parle Agro, and Bisleri in Maharashtra and Gujarat

- Southern Region: UBL, HCCB, and Tata Consumer facilities across Karnataka, Andhra Pradesh, and Tamil Nadu

- Eastern Region: Emerging importance with VBL and HCCB plants in West Bengal, Jharkhand, and Odisha

Capacity Expansion Trends

Major capacity expansion investments totaling over ₹50,000 crore are underway across the industry:

- VBL: ₹21,000 million invested in 2023 for greenfield and brownfield expansions

- HCCB: Significant investments in Gujarat, Telangana, and Maharashtra facilities

- Reliance (Campa): ₹1,000 crore investment in Bihar facility

- Amul: ₹1,000 crore annual investment in plant expansions

Technology and Sustainability Integration

Modern beverage manufacturing in India emphasizes sustainability and technology integration:

- Solar Power Adoption: HCCB’s plants in Andhra Pradesh and Telangana use solar power for 50-75% of energy requirements

- Water Efficiency: Industry-wide focus on reducing water usage ratios and implementing recycling systems

- Automation: State-of-the-art bottling lines with capacities exceeding 600 bottles per minute

Market Outlook and Growth Projections

Future Growth Trajectory

The Indian beverage market is positioned for sustained double-digit growth driven by:

- Demographic Dividend: 65% of population below age 35 providing long-term consumption growth

- Premiumization Trend: Growing preference for premium and functional beverages

- Rural Expansion: Untapped rural markets offering significant growth potential

- Health and Wellness Focus: Rising demand for low-sugar, organic, and fortified beverages